Futarchy: When the prediction market becomes a governance weapon, a governance experiment that subverts the paradigm of DAO decision-making

By Loxia

InMarch 2025, Optimism launched a landmark on-chain governance experiment. By allocating 500,000 OP tokens through the Futarchy mechanism, this 21-day social experiment not only tested the feasibility of the prediction market in the ecological governance of the public chain, but also revealed the complex tension of the evolution of decentralized decision-making mechanisms.

01、Futarchy Governance Experiment

Optimism launched a very novel Futarchy governance experiment in March, the literal translation of Futarchy is a prediction experiment, in the blockchain, Futarchy is a governance model that guides decision-making through the prediction market, using the prediction ability of the financial market and the real money input of participants to incentivize more accurate prediction and analysis. In this experiment, Optimism used Futarchy to distribute a total of 500k OP (100k * 5) of incentives to explore a new incentive distribution model for the public chain side to incentivize the development of the ecosystem, and most of the progress of the experiment has been completed, and Loxia, a member of LXDAO, as one of the participants in the experiment, expressed cautious optimism about the future of the governance method.

Futarchy proposed by MetaDAO is simply that when someone proposes a governance purpose (such as "airdrop tokens to incentivize users"), Futarchy will define two conditions: "pass" and "veto" token market. Participants need to pledge real assets in exchange for the corresponding token for trading - if they are optimistic that the proposal will push up the price of the token, they will buy the "pass" market token; Otherwise, bet on the "veto" market. In the end, the fate of the proposal is determined by comparing the weighted average prices of the two markets, and the participants can redeem the collateral assets, but the decision results directly affect the value of their holdings. This design cleverly binds individual interests to collective goals:

to make a profit, you have to dig deep into the long-term impact of the proposal on the organization's token price, rather than voting on intuition or following the herd. MetaDAO's practice shows that even if a malicious proposer tries to manipulate the market, the need to acquire "pass" tokens at a high price will outweigh the losses. MetaDAO believes that when every decision is tempered by real money, collective intelligence has a chance to overcome human weaknesses.

02, Origin of Futarchy

Futarchy is a form of government proposed by economist Robin Hanson. In this model of governance, elected officials define measures of the country's well-being, and predictive markets are used to determine which policies will have the most positive impact. The New York Times listed "Futarchy" as a buzzword in 2008. Later, the concept was also introduced into the discussion of blockchain and DAOs.

Futarchy's slogan is:

"vote on values, bet on beliefs." The meaning of this sentence is that

citizens should use democratic procedures to express "what we want" (i.e., "values").

The prediction market is then used to determine "what policies are most likely to achieve these goals" (i.e., "beliefs" – judgments about cause and effect).

Economist Tyler Cowen said: "I'm not optimistic about the future of Futarchy or whether it will succeed once it is implemented. Robin said, 'Vote on values, bet on beliefs,' but I don't think values and beliefs can be separated so easily.

Cowen argues that human values and beliefs are highly intertwined, and that it is difficult to completely separate "goals" from "ways to achieve them." For example, a person may claim to pursue social equality (values), but his support for certain policies (beliefs) is actually motivated by ideological preferences rather than rational predictions of the effects of the policies.

In other words, prediction markets cannot be completely shielded from human emotional, cognitive biases, and value-oriented interference, so Futarchy's operating mechanism may not be as rational and efficient as it can theoretically.

03 Futarchy for Optimism

The designers of the Futarchy governance experiment believe that

-

when decision-makers are rewarded and punished for their accuracy (accurate → rewarded, inaccurate → punished), they tend to make more thoughtful, unbiased decisions;

-

At the same time, a permissionless futarchy model can attract more people to participate (crowd intelligence) rather than being limited to centralized decision-making bodies.

At the same time, in order to make the experiment more open, and in order to get more data to test the experiment, the experimenter has opened the participation permission, anyone with a telegram account or Farcaster account can participate, and all predictors will get 50 OP-PLAY entry chips (it is OP-PLAY, the token has no real value, it is a fake chip only for experimentation), and the actual participants of OP governance will get more OP-PLAY chips.

So what are the prediction issues around this round of Futarchy?

If a project receives 100k OP incentives, which protocol(s) will receive the greatest TVL growth after three months.

There are 23 projects participating in Futarchy this time, and each person participating in the experiment needs to predict the TVL increment of these 23 projects after "getting the 100k OP incentive", at the beginning of the experiment, the initial predicted TVL of all projects is the same (the same starting line, as a reference, in the project selection of the test experiment), over time, the user will stake OP-PLAY and buy call options (UP) for different projects token) and put options (DOWN token), and the five projects with the highest prediction results will each receive an incentive of 100k OP.

At the end of the experiment, participants selected five projects through OP-PLAY to participate in the prediction market, and as a comparison, the Grants Council also selected its own five funded projects:

thefirst five 100K OP grants selected by Futarchy in a 21-day up-and-down game:

-

Rocket Pool: $59.4M

-

SuperForm: $48.5M

-

Balancer & Beets: $47.9M

-

Avantis: $44.3M

-

Polynomial: $41.2M

at the same time Grants Council The five selected funded projects will only be issued once if there is an overlap

:-

Extra Finance

-

Gyroscope

-

Reservoir

-

QiDAO

-

Silo

04, Limitations of the Futarchy Model in Governance

Limitations of this TVL Judgment Metric:

"If the price of ETH rises, protocols that lock up a lot of ETH will look like they are growing a lot on TVL, even if they don't do anything." — @joanbp, March 13

"We seem to be using Futarchy to decide who should receive the grant, but if the TVL growth is only a reflection of market price changes, then this metric does not reflect whether the project is making good use of the grant." — @joanbp,

the angle from which the indicators of the March 13 prediction experiment were set up is also very important:

"We should choose those indicators that – even if the participants want to 'manipulate' – can only 'win' by doing something ecologically beneficial." — @Sky, the

deviation brought by the simulated token on March 17 (and the deviation will also occur if the real token value is insufficient)

"This is 'fake money', not 'real money'. A lot of people will bet on both sides at the last minute, just to not lose. —

@thefett, March 19

*41% of participants hedge their risk at the end of the day (bet on both sides to avoid losses)

"I feel like I'm not bringing any particular insights, but rather diluting the influence of those who really understand the project."

— @Milo, the user experience on March 20

was poor and affected the effectiveness of the game:

thesuccess of the prediction market depends heavily on the depth of user engagement. However, the threshold for this experiment experience is high, the information is opaque, and the operation is cumbersome, which greatly affects the judgment and participation of the participants.

Common feedback from users includes:

-

Not knowing how many tokens there are in total.

-

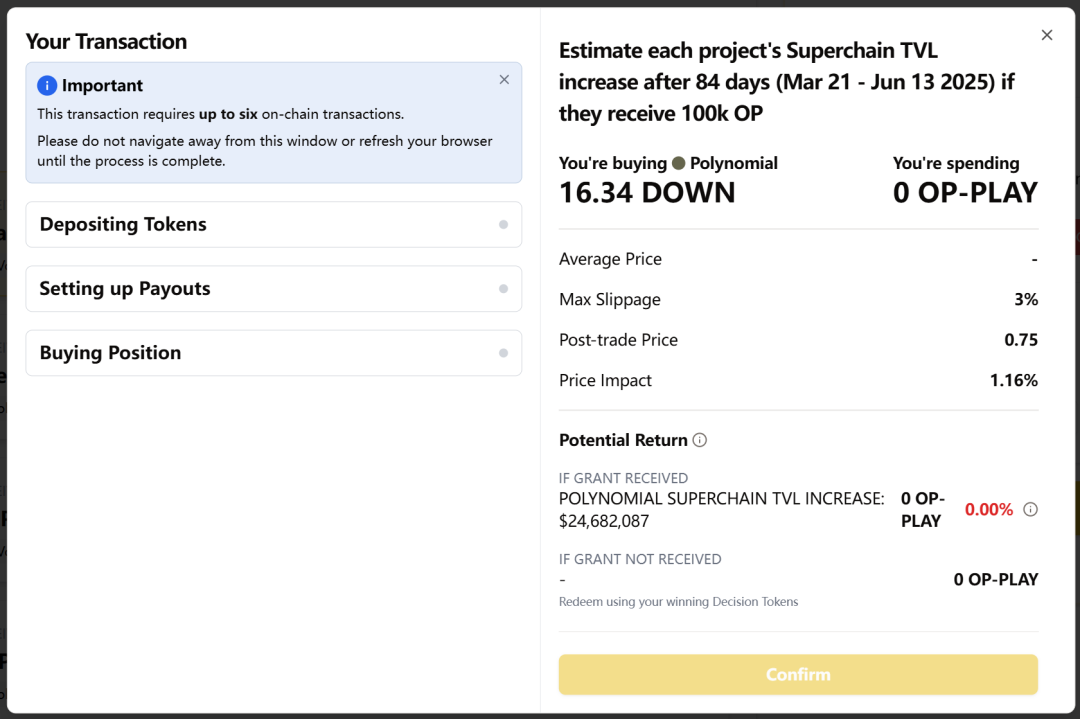

A single bet requires 6 on-chain interactions. (So I didn't do a few trades in this experiment, the interface is too complicated)

-

I can't explain whether the wrong item is losing money.

-

The logic of profit and loss in the leaderboard is incomprehensible.

"I THOUGHT PLAY WAS USED AT FIRST, BUT IT TURNED OUT THAT EVERY ITEM WAS RESET, AND I COULDN'T FIGURE OUT HOW MUCH I WAS SPENDING IN TOTAL." — @Milo, March 20

"One prediction to sign six deals is a bit too much." — @Milo, March 20

"I can't read the leaderboard, sometimes I feel like I'm supposed to be profitable, and it turns out to be a 46% loss." — @joanbp, on March 19,

Butter's official data report showed that the total

transaction volume of this experiment was-

5,898, but 41% of the addresses only participated in the last three days, indicating that the user learning cost is too high.

-

A single prediction requires 6 on-chain interactions (see screenshot of the interface), resulting in an average of only 13.6 transactions per person.

-

Despite 2,262 visitors, the conversion rate was only 19%, and the OP governance contributor participation rate was only 13.48%

-

45% of the projects did not disclose their plans to the forecasters, and the information asymmetry led to prediction bias (e.g., the Balancer forecast exceeded the project's self-estimate by $26.4M)

05,

Summary1. The establishment of game indicators will have a decisive impact on the Futarchy experiment

,and good indicators should have:

-

Measurability: clear and easy to verify data;

-

Correct direction: can guide participants to do things that "promote the positive development of the system even if it is to win money";

-

Not easy to gamify: It is difficult to be "bigger and stronger" by simple financial skills or price fluctuations.

For example, in this Futarchy experiment, the TVL in US dollars is very susceptible to fluctuations in the price of mainstream currencies such as ETH, making the prediction more like "betting on the price of the coin" rather than assessing who really has the ability to grow.

According to the official report issued by Butter, the interim TVL data as of April 9, 2025 has exposed the limitations of the metrics:

-

Rocket Pool (forecast TVL growth of 59.4M) Actual TVL growth of 59.4M, actual TVL growth of 0

-

SuperForm (forecast 48.5M) actually fell by 1.2M

-

Balancer & Beets (forecast 47.9M) actually fell by 13.7M

The total actual TVL of all Futarchy selected projects reached $15.8M, while the Grants Council selected projects during the same period:

-

Extra Finance (forecast 39.7M) real growth of 8M

-

QiDAO (forecast 26.9M) real growth of 10M

This verifies the community's suspicion that the TVL indicator is strongly correlated with the market price and does not effectively reflect the real operational capability of the project.

2. Futarchy's "Best Forecaster" results are not completely objective

-

In this experiment, it is more a reflection of the participants' OP-PLAY trading ability than the selection of "prediction ability", because in this experiment, all the targets have a large daily rise and fall, and the participants have a considerable room to operate (anonymous account @joanbp reached the top through high-frequency trading (406 transactions/3 days)).

-

In the final OP-PLAY trade win rate leaderboard, Badge Holders, as a recognized OP ecosystem professional, has the lowest group win rate.

-

Only 4 of the top 20 forecasters hold OP governance status (skydao.eth/alexsotodigital.eth, etc.3

. Predicting the paradoxes that influence decision-making:

The nature of Futarchy is that prediction is decision-making, and collective expectations have a direct impact on the outcome (e.g., which project in this experiment receives a grant). This is different from the general prediction market, which purely predicts external events, creating some unique dynamic challenges. As discussed in the OP forum, a voter has two orientations in Futarchy:

first, to follow the exile to stake popular projects to ensure that they are funded (their own predictions are correct but not necessarily high returns, because most people bet on them);

Second, if the undervalued project is selected by theunusual, the personal benefit is greatest if it turns out that the minority is right. This dual nature of voting and betting makes participants a little confused. At the same time, when the prediction itself shapes the future (because the flow of money affects the development of the project), Futarchy has a certain cycle of self-realization or self-defeat: everyone presses a project well, and resources are given to it, and it naturally has a better chance of success; On the other hand, even if it could have succeeded, it failed because it did not have the resources. This closed loop requires the Futarchy experiment to be carefully interpreted for its prediction accuracy and designed to mitigate the bias of this self-proving loop.

In this Futarchy experiment, we see not only how governance mechanisms are being "gambled", but also the potential of Degen in the prediction market – they are no longer just profit-seeking passers-by, but potential professional governors. Only when the institutional design can anchor Degen's energy to the public goal, let speculation become co-construction, and let betting become judgment, will Futarchy have a chance to activate the regenerative governance spirit (Regen) that belongs to Web3. This experiment awakens the possibility that governance does not have to be puritanical rational negotiation, but can also be deeply gamified consensus formation. Awakening Degen's Regen bloodline may be the evolutionary direction of DAO governance in the future.