With a rise of nearly 50% in a week, will ENA be ETH's biggest beta?

Original | Odaily Planet Daily (@OdailyChina)

Author|Azuma(@azuma_eth)

ETH is finally hardening!

With the continuous upward surge of the "altcoin leader" ETH, the altcoin market has shown signs of recovery, and mainstream projects in the Ethereum ecosystem such as Ethena (ENA), Lido (LDO), Curve (CRV), and Frax (FRAX) have risen even more, among which ENA once exceeded $0.5 in the short term, with a weekly increase of nearly 50% (this is still based on the increase after a round of pull-up due to the launch of Upbit more than a week ago by ENA), in a number of so-called "ETH" beta".

Focusing on the reasons for ENA's strong rise, based on the analysis of all parties, we believe that it can be attributed to the following four reasons.

Reason 1: ETH has been boosted

First of all, most of Ethena's business is still focused on the Ethereum ecosystem (a small part of USDe has flowed to ecosystems such as Solana through cross-chain forms), and Ethena is also one of the few star projects that have emerged in the Ethereum ecosystem in the past two years, so it is not an exaggeration to say that it is "Ethereum descendant".

Similar to the aforementioned currencies such as LDO and CRV, the rise of ETH will inevitably boost mainstream projects in the ecosystem, which is an essential prerequisite.

However, this does not explain why ENA has been able to lead the "Ethereum concept coin" recently, and the real reasons are the following three points.

Reason 2: The business model returns to the positive flywheel

To understand this reason, you need to first write about Ethena's business model.

In short, Ethena is an interest-bearing stablecoin project focusing on "futures and cash arbitrage", and its stablecoin USDe will be collateralized by an equal amount of spot long and contract shorts, and its income mainly comes from "pledge income of spot longs" and "funding rate income of contract shorts", of which the first income does not fluctuate too much, and the second income is the key to the operation of the protocol's business.

Although in the long run, the funding rate will account for the majority of the time when the funding rate is positive (that is, the overall contract bears will get positive rate returns), but when the market sentiment is pessimistic, the rate will continue to fall or even show a negative value - this will seriously affect Ethena's protocol revenue capacity, and even short-term losses.

-

Odaily Note: For the basic concept of Ethena and the impact of fee fluctuations, please refer to "A Brief Analysis of Ethena Labs: Valuation of $300 Million, a Stablecoin Disruptor in the Eyes of Arthur Hayes", "After the Crash, How Does Ethena (USDe) Perform Under Negative Fees?" 》。

For a long time, due to the overall lack of optimism in the market, the fees in the contract market have always been low, which has also led to the long-term unsatisfactory yield of Ethena's protocol revenue level and sUSDe (staked interest-bearing version of USDe).

However, with the recent rapid recovery of the market (especially ETH's market, which is the main target of Ethena's term arbitrage), the contract fee level has also been climbing - the Ethena page shows that the current average rate of the protocol is about 16% annualized.

The average yield of sUSDe in the past two weeks has increased from about 5.59% to 9.74%, which has also directly attracted more capital inflows - the on-chain shows that the issuance scale of USDe has grown to about $6.1 billion, a record high.

In short, this is a positive flywheel: the market is warming ➡️ up, the sentiment of going long is rising ➡️, the rate income is ➡️ rising, the income of stablecoins is improving ➡️, the inflow of funds is increasing ➡️, the scale of stablecoin issuance is growing ➡️, the fundamentals of the protocol are improving ➡️, and the price of the coin is strongly supported......

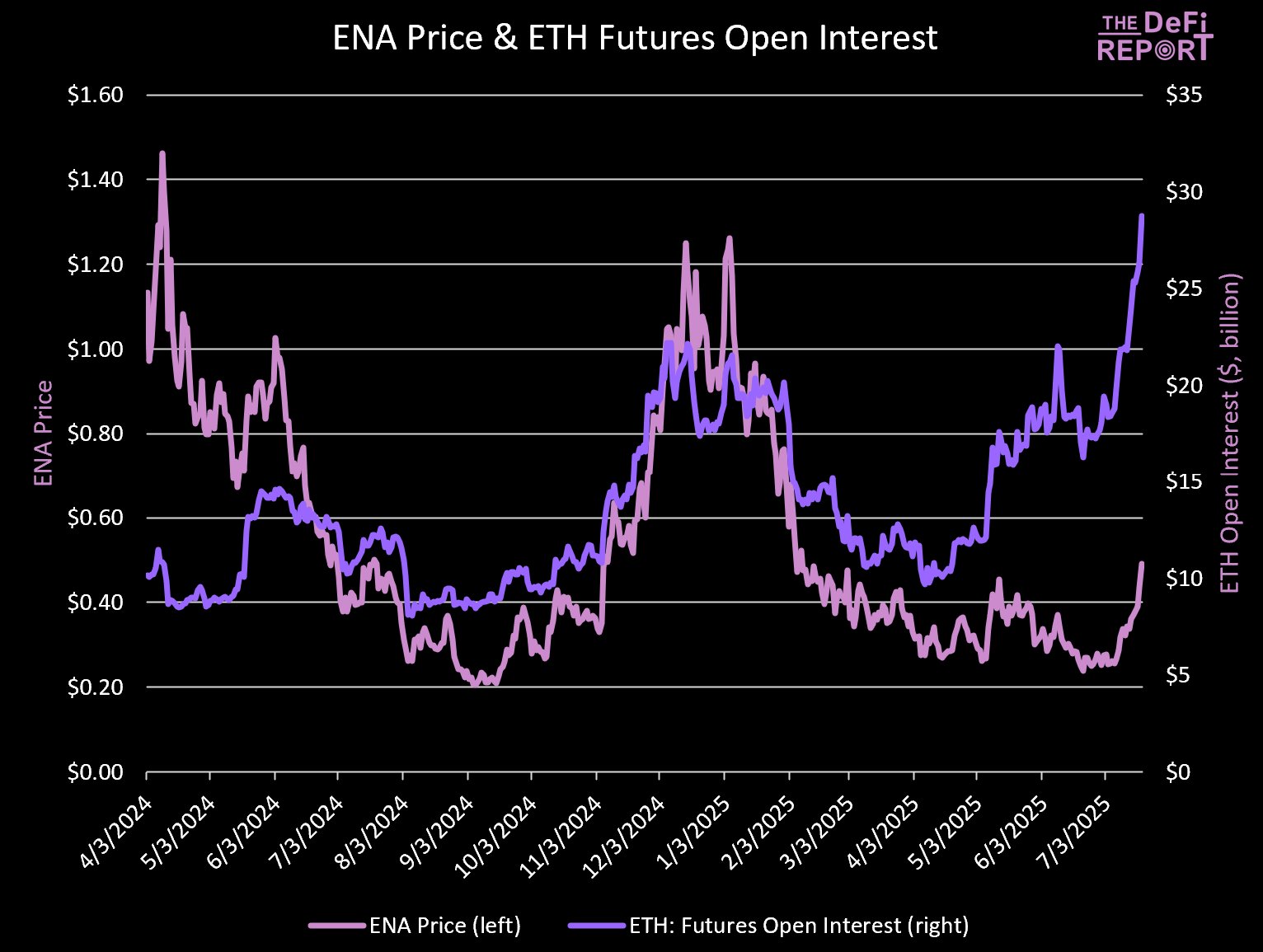

The following chart can more intuitively illustrate this logic, as the price rise and fall of ENA is significantly synchronized with the increase or decrease in the contract size of ETH.

Reason 3: The stablecoin bill was passed, and the sector as a whole was good

Another major benefit of Ethena recently is the passage of the Stablecoin Act.

In the early morning of July 19, Beijing time, U.S. President Trump officially signed the GENIUS Act in the East Room of the White House, which means that this bill focusing on the development of the stablecoin industry has passed through all legislative processes and officially became a law to take effect.

-

Odaily Note: For details, see "Historic Moment: Trump Officially Signs the GENIUS Act".

Although USDe may not meet the requirements of the GENIUS Act that "stablecoins must be fully backed by US dollars or other highly liquid assets at a 1:1 ratio", Ethena is already ready to do so - at the end of last year, Ethena launched a new stablecoin product USDtb backed by BlackRock's BUIDL, which will be backed by a 1:1 ratio using cash or cash equivalent reserves, as of the publication of USDtb The issuance size has also grown to $1.46 billion.

To put it simply, Ethena now walks on two legs, with USDe specializing in the crypto-native market and USDtb specializing in the compliant institutional market.

Reason 4: ENA's "fee switch" expectations

The potential "fee switch" activation is another reason for ENA's recent rise. The so-called "fee switch" is a common term used in DeFi protocols to determine whether to allocate protocol revenue to the protocol's native token (ENA in this context). If this switch can be turned on, it will directly boost ENA's ability to capture value.

In previous community votes, Ethena has clearly defined five conditions for activating the "fee switch" as follows.

-

✅USDe Circulation: Required to exceed $6 billion, currently $6.1 billion, has been met.

-

✅ Cumulative Agreement Revenue: Over $250 million required, currently $431.31 million, met.

-

❌ Exchange adoption: USDe is required to be listed in 4 of the top 5 exchanges by derivatives trading volume, and currently 3 are not met.

-

✅ Reserve Fund: Requires more than 1% of USDe supply, met the target.

-

❌The spread between the yield of sUSDe and the benchmark interest rate is 5.0-7.5%, the current spread with Aave USDC is 3.03%, the spread with US Treasury bonds is 2.48%, and the spread with sUSDS is 2.05%, which is not up to standard.

It can be seen from the above that three of the five requirements are already eligible. Considering the recent trend of higher rates, sUSDe's yield is also rising in tandem, which will help achieve the fifth condition, and the third requirement is also left with only one exchange to integrate.

It doesn't look too far away from the activation of the "fee switch", and the market may choose to bet ahead at this time.

Will ENA be ETH's biggest beta?

In addition to the above reasons, another thing to note is that BitMEX founder Arthur Hayes, who previously "smashed while smashing" ENA when it was at a high of above $1, seems to be quietly making up for his position. On-chain analyst Ember monitored last week that Arthur purchased a total of $1.505 million worth of ENA through multiple channels in a single day.

What Arthur said cannot be fully believed, but what he did still has some reference significance......

-

Odaily Note: You can refer to reading "When Arthur Hayes Suddenly Milks the Coins You Buy, You Should Be Careful".

Based on the above reasons, it is foreseeable that ENA's fundamental growth trend and value capture expectations will continue in the next period of time, which may support its continuation of its current price trend. At a time when ETH is gaining momentum, perhaps ENA will be a potential beta option.