Circle's IPO is questioned: the valuation is almost halved, and the desperate monetization attempt under the pressure of profits?

By Nancy, PANews

After years of unsuccessful IPO preparations, Circle, the issuer of the stablecoin USDC, recently submitted an application to the SEC to be listed on the New York Stock Exchange. However, issues such as valuations nearly halved, high dependence on U.S. Treasuries for revenues, and high share losses have also raised questions about Circle's business prospects.

The valuation was almost halved, and the shares were sold to Coinbase in exchange for the full issuance rights of USDC

The day before the U.S. House of Representatives plans to amend and vote on the stablecoin regulatory bill GENIUSAct, SEC website documents show that Circle filed an S-1 file with the SEC to conduct an initial public offering under the ticker symbol "CRCL" and apply for listing on the New York Stock Exchange. Meanwhile, Circle has hired JPMorgan Chase and Citibank to help with its IPO, both of which were also members of the financial advisory team for Coinbase's IPO.

However, Circle does not disclose in detail the specific number of shares to be issued and the target price range in this prospectus. However, Circle's valuation has changed several times in response to market conditions and its size, from $4.5 billion in 2021 when the SPAC merger was traded, to $9 billion in 2022 when the merger agreement was amended, and then to about $5 billion in the secondary market in 2024. According to Forbes, Circle's target valuation in this traditional IPO plan is between $4 billion and $5 billion, which has shrunk by nearly half from its peak.

Circle had full control of the USDC issuance rights prior to the IPO. According to The Block, Circle acquired the remaining 50% stake in the Centre Consortium in 2023 for $210 million worth of shares, which was previously held by Coinbase. The Centre Consortium is a joint venture responsible for the issuance of the USDC stablecoin, which was jointly established by Coinbase and Circle in 2018.

"In August 2023, at the same time as entering into the cooperation agreement, we acquired the remaining 50% equity interest in Centre Consortium LLC from Coinbase," Circle disclosed in the "Material Transaction" section of the prospectus. "The consideration for the transaction was paid for approximately 8.4 million shares of Circle common stock, totaling $209.9 million at fair value. Upon completion of the acquisition, Centre became a wholly owned subsidiary of Circle and was dissolved in December 2023 and its net assets were transferred to another wholly owned subsidiary of Circle. Coinbase also disclosed that it acquired a Circle stake that was granted by agreement rather than a cash purchase. This also means that Circle will use the company's shares in exchange for full control of USDC, and the deal will not directly affect Circle's cash flow.

In fact, Circle began preparations for an IPO as early as 2021, reaching a merger agreement with SPAC firm Concord Acquisition to list through the SPAC route, but the deal was delayed due to lack of SEC approval and finally announced its termination at the end of 2022. In January 2024, Circle again revealed that it had filed an IPO application in secret and said it would do so after the SEC completed its review process.

Compared with previous attempts, the background of this application has changed significantly: now the stablecoin market has achieved a qualitative leap in size, the growth momentum is strong, and the influence of stablecoins, including USDC, in global finance is increasing; At the same time, the United States has a positive attitude towards compliant stablecoins, creating more development space for the development of the stablecoin track, including JPMorgan Chase, PayPal, Visa, Fidelity and Ripple and other giants are laying out stablecoins, and the Trump family project WLFI also plans to promote stablecoins. At the same time, crypto companies such as Kraken, eToro, Gemini, and CoreWeave are all looking to IPO amid the growing clarity of crypto regulatory policy in the United States.

Revenues are highly dependent on U.S. bonds, and Coinbase's high commissions eat up profits

However, Circle's IPO prospects are facing multiple doubts, with its core business model and profitability sparking heated debates.

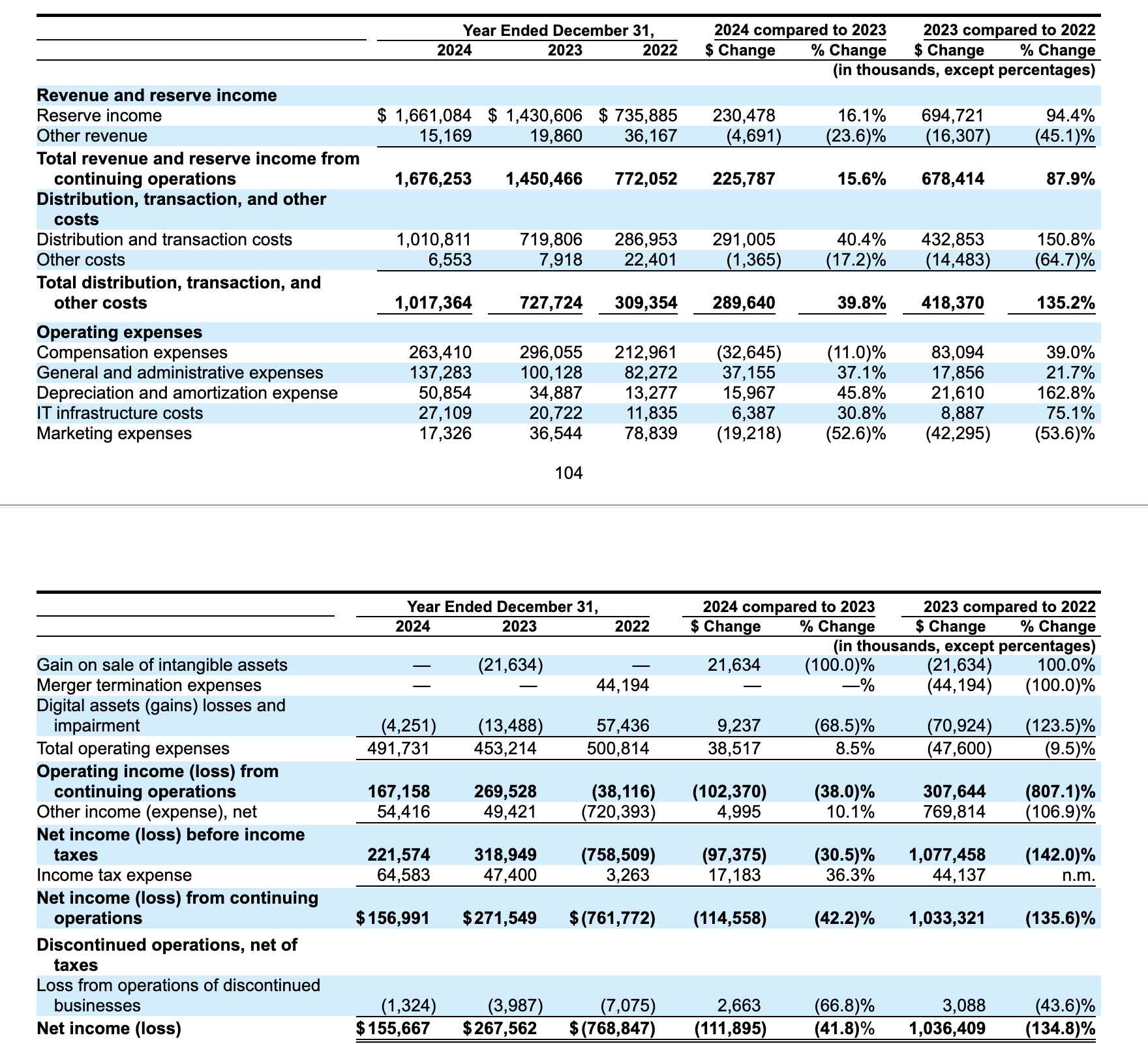

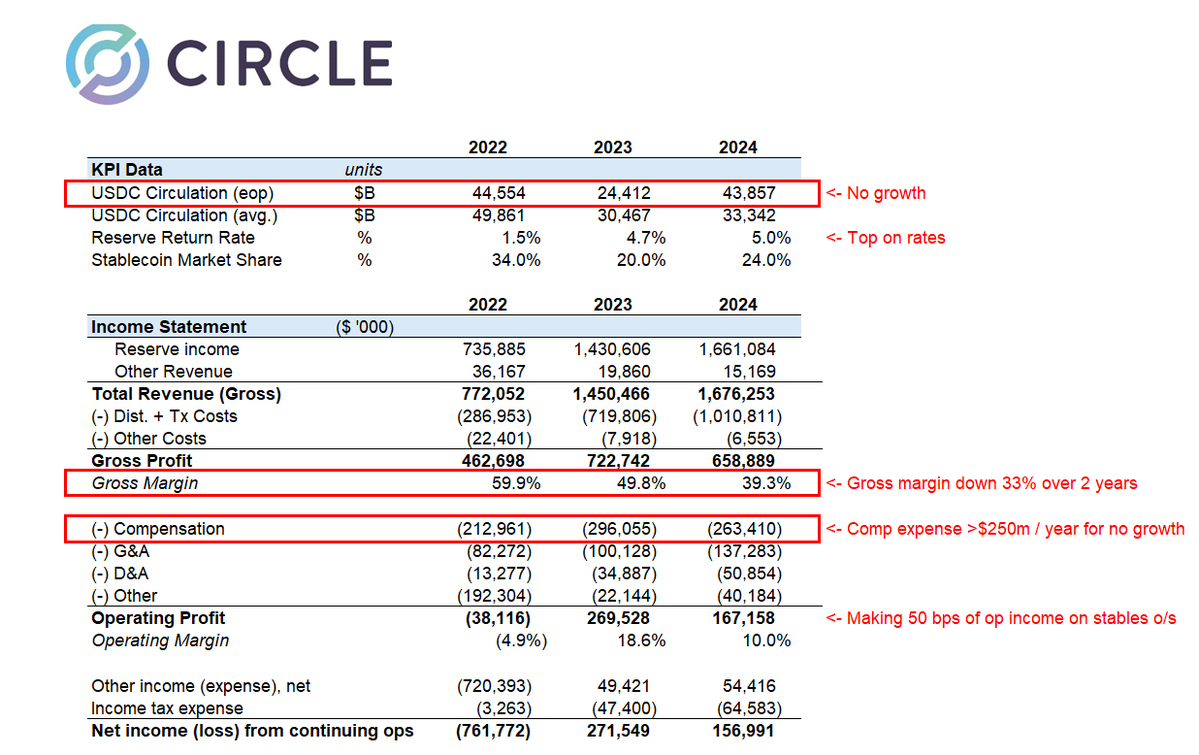

First, Circle's income is highly dependent on US Treasury yields, a model that looms precarious in anticipation of Fed rate cuts. According to the IPO filings, Circle's total revenue in 2024 will be $1.676 billion, and the increase in income will mainly come from reserve income, that is, interest income generated by USDC reserves, accounting for more than 99% of total income, and this part of interest income mainly comes from U.S. Treasury bonds. In a sense, Circle's revenue model is like a Treasury arbitrage game.

Second, high distribution costs further erode Circle's profits. Circle's net profit in 2024 will be $155.67 million, down 41.8% from 2023. Behind this decline is a significant rise in distribution and transaction costs, with Circle spending a total of $1,010.8 million in 2024, accounting for 60.7% of total revenueThis is an increase of 40.4% compared to 2023. Among them, Coinbase is the main distribution platform for USDC. According to Coinbase's previous financial report, in Q4 2024 alone, Coinbase will receive $225.9 million in revenue from USDC, and it is expected to receive about $900 million for the whole year. This means that Circle is spending more money to keep the USDC ecosystem in circulation, but revenue growth has not kept pace.

In fact, according to the S-1 listing documents, Coinbase, as its core partner, receives a 50% share of the remaining earnings from the USDC stablecoin reserves. Coinbase's share ratio is directly pegged to the amount of USDC held on its exchange. The document states that when the USDC hosted by the Coinbase platform increases, its share ratio increases accordingly; Otherwise, it will decline. In 2024, the proportion of USDC held by the Coinbase platform has increased significantly from 5% in 2022 to 20%.

Matthew Sigel, head of digital asset research at VanEck, said that despite the increase in overall revenue, the significant increase in Circle's costs in distribution and trading had a negative impact on its EBITDA (earnings before interest, taxes, depreciation and amortization) and net profit. Circle also warned that Coinbase's business strategy and policies directly affect USDC's distribution costs and revenue share, and that Circle has no control over or regulation of Coinbase's decisions.

However, in an effort to reduce its reliance on Coinbase, Circle has also been expanding its global partnerships in recent years, including partnerships with global digital finance companies such as Grab, Nubank, and Mercado Libre.

But in the opinion of Omar Kanji, a partner at Dragonfly Capital, there is nothing to look forward to in Circle's IPO application, and it is completely impossible to understand how it was priced to $5 billion. Interest rates have been severely eroded by distribution costs, core revenue drivers have peaked and begun to decline, valuations are ridiculously high, and annual compensation expenses exceed $250 million. It feels more like a desperate monetization attempt to cash out and run away before the big players get in.

"As Nubank, Binance and other large financial institutions begin to work with Circle, it remains unclear how the market will assess their distribution network and Circle's net profit margins. How the market embraces Circle will depend in part on how they deliver that message to investors, how they execute the story they tell the market, which stablecoin bill wins, and most importantly, how the market evolves and how stablecoins are adopted at scale. If the dominant position is USDC, then even if their rake percentage drops, Circle can get a higher valuation multiple, because the market potential that they can scale is huge. In any case, a few points are clear: 1) the revenue sharing model with B2B partners will be here to stay for a long time; 2) As the overall stablecoin market grows, issuers' profit margins will shrink; 3) Issuers need to diversify their revenue streams and rely on more than just net interest margins. Wyatt Lonergan, Partner at VanEck Ventures, said.

Overall, although the improved crypto regulatory environment in the United States and the boom in the stablecoin track have provided it with a listing window, it is still unclear whether it will be able to further establish its competitiveness with IPOs under the dual pressure of the Fed's interest rate cut expectations and soaring promotion costs.